Inflation Triggering Record Credit Card Usage

Working people were forced to rack up over $46 billion in credit card debt between April and June to afford necessities.

A portion of monthly subscriptions goes to groups supporting our unhoused friends and neighbors. Please consider subscribing.

The financial crunch caused by inflation hitting a 40-year high has led to a record credit card debt increase in the United States.

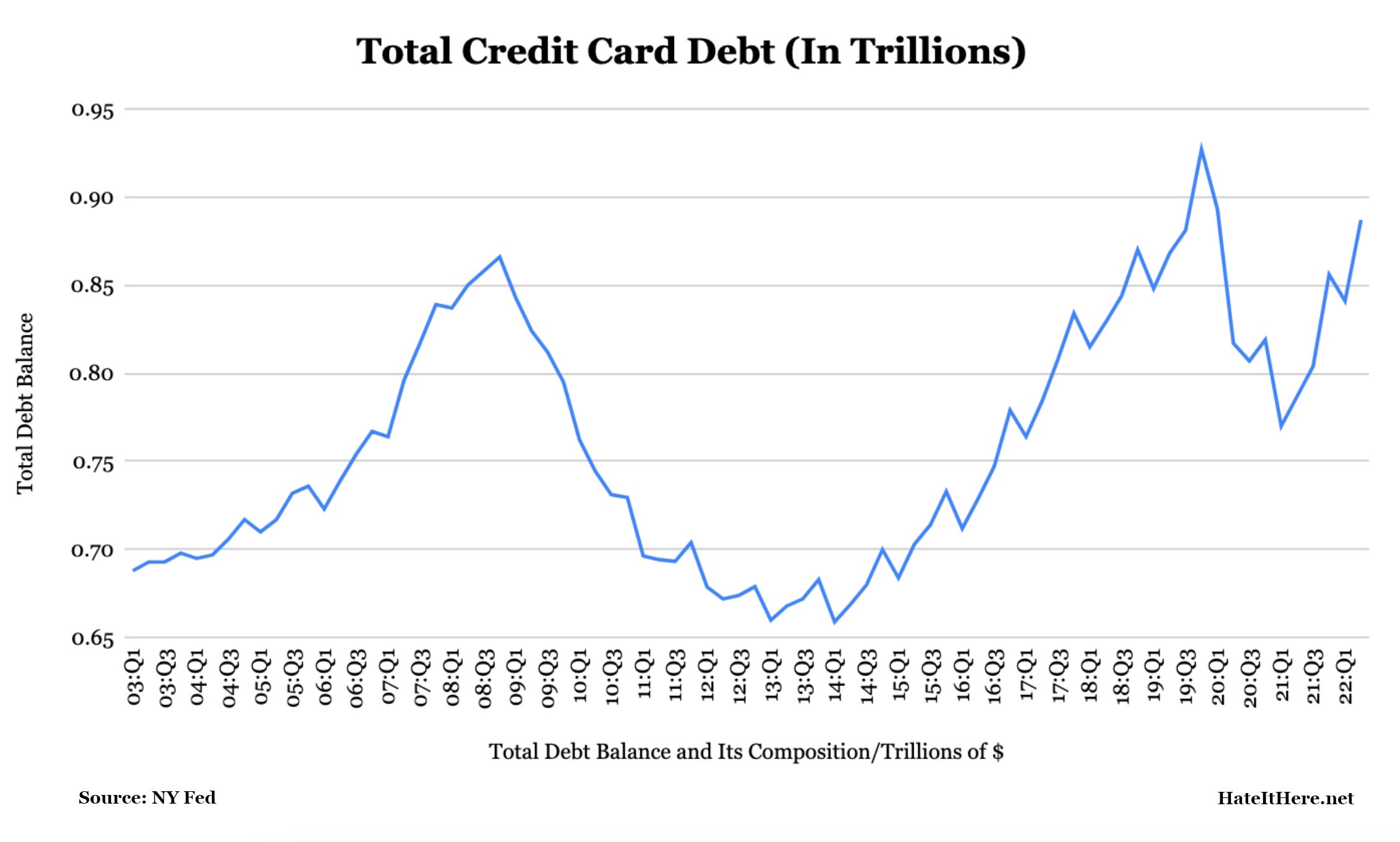

Americans racked up $46 billion in credit card debt between April and June (Q2) this year, bringing the total credit card debt burden to $890 billion, up nearly 6% from Q1 this year and a record increase of 13% compared to Q2 2021. Over the past year, cumulative credit card debt has risen by over $100 billion.

“The 13% year-over-year increase marked the largest in more than 20 years,” the New York Federal Reserve stated in its Quarterly Report On Household Debt and Credit.

In June, I wrote about how 75% of middle-income families said their wages are falling behind inflation, according to a recent report from Primerica and Change Research. 77% say they’re expecting and preparing for a recession, with 71% already cutting back on spending to help make ends meet. Working people have never lost this much purchasing power through disposable income in one year and, as a result, are increasingly racking up credit card debt to afford essentials. Just 14% of people surveyed said their credit card bills have decreased over the last three months. Over 40% of Americans expect to add to their credit card debt to deal with rising costs.

Because so many people are finding it necessary to rely on credit to stay afloat, 12.7 million new credit cards and accompanying lines of credit were issued to Americans in Q2, bringing the total number of accounts to over 549,870,000. These new accounts constitute a 7.4% year-over-year increase in new accounts.

At the same time, interest rates on that debt are rising, making it harder for working people to get out of debt. In June, the national average APR, or average percentage rate, was just under 17%. Due to the Federal Reserves interest rate hikes to “counter inflation,” analysts projected those rate increases would be passed onto consumers in the form of higher APRs. They were right, and the average is close to exceeding 18%, according to Bankrate. That is, however, if you have decent credit—and millions of Americans have “subprime” or “bad” credit, typically borrowers with credit scores in the mid-to-low 600s or below. If you fall into one of those categories, the national average APR is now over 27%, up 2% from just 6 months ago. (It’s important to remember that credit scores have only been around since 1989 when FICO scores were introduced.)

Total household debt exceeded $16 trillion for the first time ever during Q2, fueled largely by mortgage debt, which has seen a nearly $1 trillion increase year-over-year. The total mortgage debt in the United States now stands at $11.39 trillion. The next largest debt burden is student loans, which, due to some tinkering around the edges by the Biden administration in the form of forgiveness for defrauded students, is now $1.59 trillion.

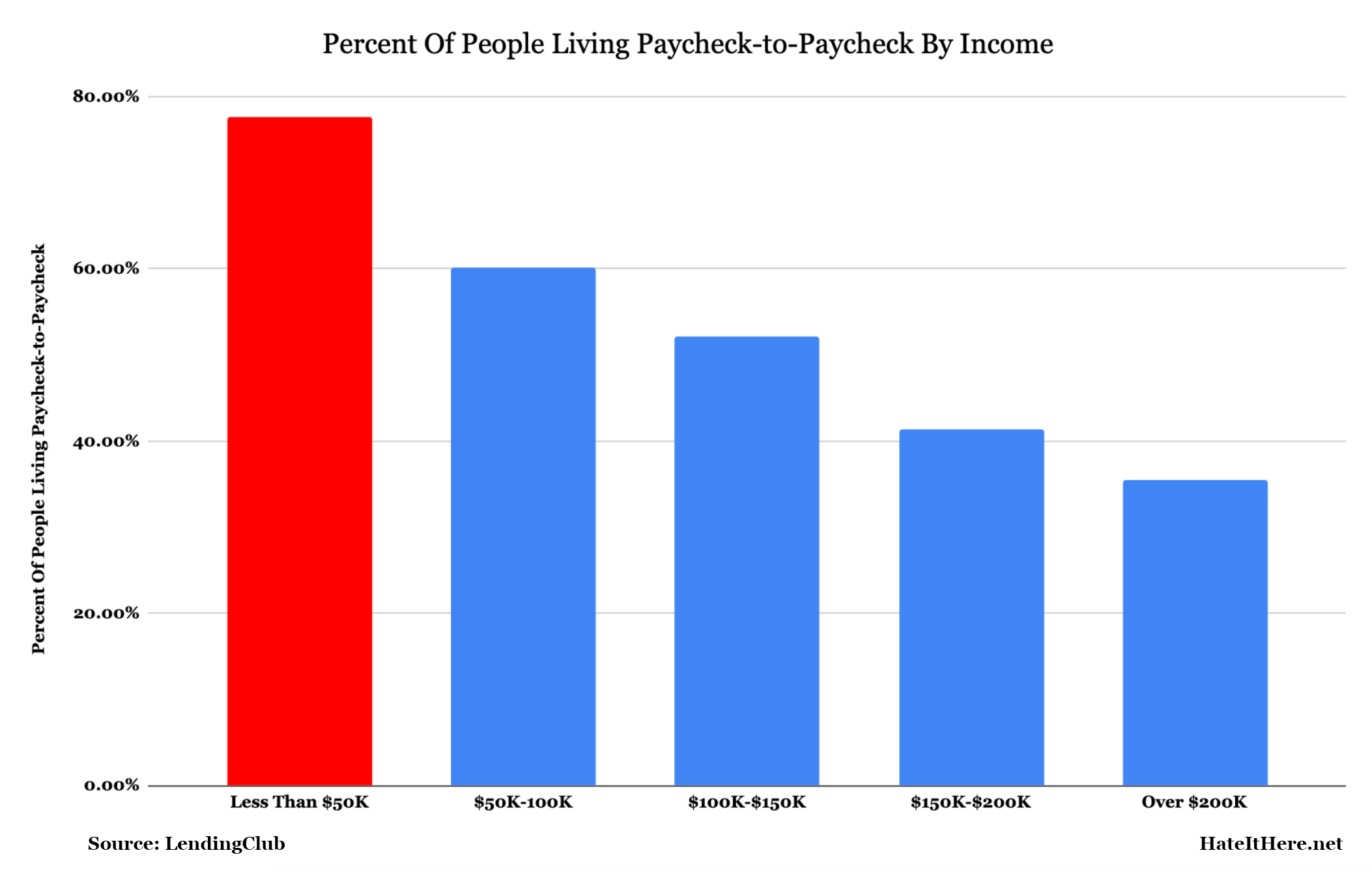

It’s extremely difficult to survive as a working person in the United States. Rent prices are growing four-times faster than income, and the national median rent exceeded $2,000 in May for the first time ever. Gas prices hit record highs over the past few months, which led to record profits for big oil. As Americans struggled at the pump because of big oil’s price gouging between April and June, Chevron, Exxon and Shell reaped a combined profit of $46.22 billion. Overall, these three oil giants have accumulated over $70 billion in profit during 2022, a 275.6% increase from this time last year. And corporate greed across the board has led to a 70-year high in corporate profits. These problems—and myriad others that continue to beat down an already beleaguered working class—have created an economy where 203 million of Americans, or 61%, are living paycheck-to-paycheck, including 77.6% of people who make under $50,000. This is unsustainable.

Thank you for reading. If you enjoyed this piece, please share it and leave a comment. And if you’d like to subscribe to this Substack, can do so below. A portion of proceeds from monthly subscriptions goes to groups supporting our unhoused friends and neighbors.

Photo courtesy of Nick Youngson, CC BY-SA 3.0, Alpha Stock Images

Very important piece and I feel like this will only get worse. Your focus on the debt being for *necessities* is so so important in the overall discussion. Thanks, Jordan! ~ Jenn

The implication is that the consumer is tapped out, and increasing debt default rates will show up this winter as the economy slows.